Key Takeaways

Table of Contents

- The Most Popular Rule — Save 20% of Your Income

- What 20% looks like by income level

- What If You Cannot Save 20% Right Now?

- The progressive savings approach

- How Much Should You Save by Age?

- In your 20s — build the foundation

- In your 30s — accelerate your savings

- In your 40s — maximise and protect

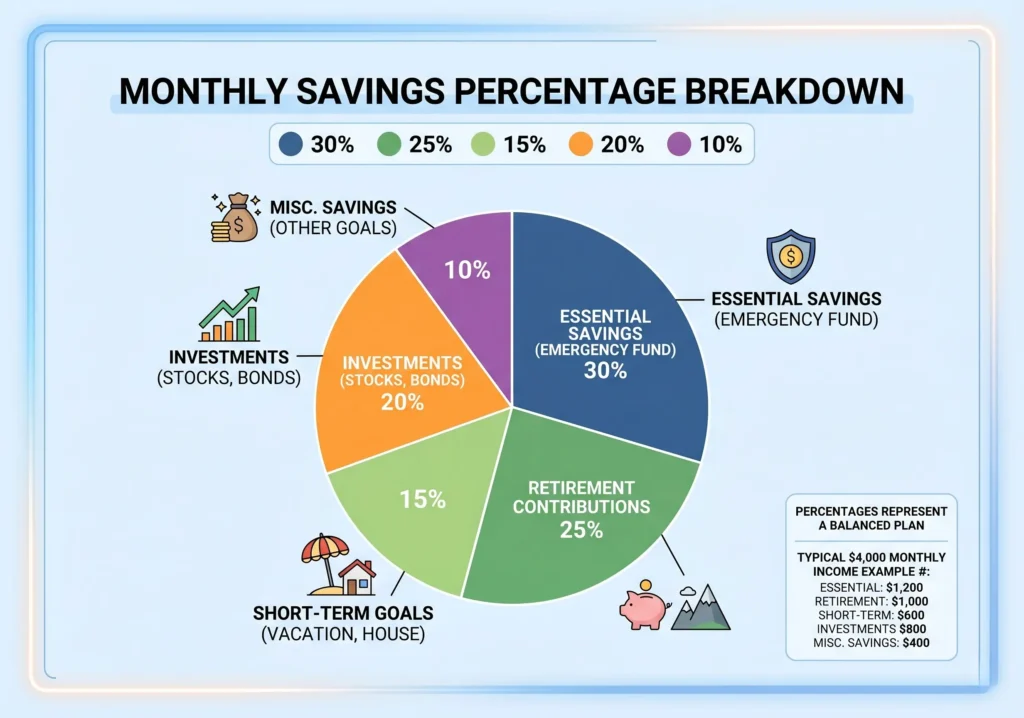

- How to Divide Your Monthly Savings Across Different Goals

- Bucket 1 — Emergency fund (first priority)

- Bucket 2 — Retirement savings (second priority)

- Bucket 3 — Specific goals (third priority)

- How to Actually Hit Your Monthly Savings Target

- Automate your savings on payday

- Review your budget every month

- Treat your savings like a fixed bill

- Factors That Should Affect How Much You Save

- Increase your savings rate when

- It may be acceptable to temporarily reduce your savings when

- Common Mistakes People Make With Monthly Savings

- Saving what is left instead of saving first

- Keeping all savings in one account

- Setting a savings goal with no deadline

- Final Thoughts

- Having 3–6 months of expenses saved as an emergency fund should be your first goal before anything else

- The most widely recommended rule is to save at least 20% of your take-home pay each month

- If 20% is not realistic right now, start with 5–10% and increase it gradually

- Your savings rate should change based on your age, income, and current financial goals

- Automating your monthly savings is the single most effective habit you can build

One of the most common personal finance questions people ask is how much money they should save each month. The honest answer is — it depends. It depends on your income, your goals, your age, and where you are in your financial journey. This guide breaks it all down so you can set a monthly savings number that is realistic, meaningful, and actually moves you forward.

The Most Popular Rule — Save 20% of Your Income

The most well-known savings guideline is the 50/30/20 rule. It works like this:

- 20% goes to savings and debt repayment

- 50% of your take-home pay goes to needs — rent, food, utilities, transport

- 30% goes to wants — dining out, entertainment, hobbies, subscriptions

The 20% savings target is a solid benchmark for most people. It covers your emergency fund, retirement contributions, and specific savings goals like a house or car — all at the same time if you divide it correctly.

What 20% looks like by income level

- Take-home pay $2,000/month → save $400/month

- Take-home pay $3,000/month → save $600/month

- Take-home pay $4,000/month → save $800/month

- Take-home pay $5,000/month → save $1,000/month

- Take-home pay $6,000/month → save $1,200/month

If these numbers feel out of reach right now, do not worry. The sections below explain how to adapt this to your real situation.

What If You Cannot Save 20% Right Now?

The 20% rule is a goal — not a requirement. If your income is tight or your expenses are high, saving 20% immediately may not be realistic. That is completely normal and does not mean you are failing.

The progressive savings approach

Start with whatever percentage you can manage — even 3% or 5% is better than zero. Then increase your savings rate by 1% every time you get a pay rise, cut an expense, or reduce a debt.

Here is how this looks over time:

- Month 1: Save 5% ($150 on a $3,000 income)

- Month 6: Increase to 8% ($240)

- Month 12: Increase to 12% ($360)

- Month 24: Reach 20% ($600)

Small, consistent increases compound into major progress. The key is to never decrease your savings rate — only ever increase it.

How Much Should You Save by Age?

Your age plays a big role in how much you should be saving and what you should be saving for. Here is a rough guide by life stage.

In your 20s — build the foundation

Your 20s are about establishing habits more than hitting specific numbers. Aim to:

- Build a 3-month emergency fund as your first priority

- Save at least 10–15% of your income

- Start contributing to a retirement account even if it is a small amount

- Avoid high-interest debt wherever possible

In your 30s — accelerate your savings

By your 30s your income is typically higher and your savings habits should be stronger. Aim to:

- Have 1–2 times your annual salary saved in retirement accounts by age 35

- Save 15–20% of your income consistently

- Have a fully funded emergency fund of 3–6 months of expenses

- Be actively saving for specific goals — house, car, children’s education

In your 40s — maximise and protect

Your 40s are about maximising contributions and protecting what you have built. Aim to:

- Have 3 times your annual salary saved in retirement by age 45

- Maintain your 20% savings rate or increase it if possible

- Pay down your mortgage aggressively if you own a home

- Diversify your savings across different account types

How to Divide Your Monthly Savings Across Different Goals

Knowing how much to save is one thing. Knowing where to put it is another. Most financial advisors recommend splitting your savings across three buckets.

Bucket 1 — Emergency fund (first priority)

Before anything else, build an emergency fund of 3–6 months of living expenses. This is your financial safety net. Until this is fully funded, it should receive the majority of your monthly savings.

Bucket 2 — Retirement savings (second priority)

Once your emergency fund is in place, prioritise retirement contributions. If your employer offers a match on pension or 401k contributions, always contribute at least enough to get the full match — it is free money you should never leave on the table.

Bucket 3 — Specific goals (third priority)

After your emergency fund and retirement contributions are covered, the remaining savings go toward specific goals — a house deposit, a car, a holiday, or anything else you are working toward.

How to Actually Hit Your Monthly Savings Target

Knowing your number is the easy part. Consistently saving it is where most people struggle. These habits make it significantly easier.

Automate your savings on payday

Set up an automatic transfer to your savings account on the same day your salary arrives. This is the single most impactful thing you can do. When the money is moved before you see it, you naturally adjust your spending to what is left.

Review your budget every month

Spend 15 minutes at the end of each month reviewing what you spent and whether you hit your savings target. If you underspent — move the extra into savings immediately. If you overspent — identify why and fix that one thing for next month.

Treat your savings like a fixed bill

Your monthly savings transfer is not optional — it is a bill you pay to your future self. Frame it this way and it becomes non-negotiable rather than the first thing cut when money feels tight.

Factors That Should Affect How Much You Save

Your savings rate is not fixed forever. These life changes should prompt you to review and adjust your monthly savings amount.

Increase your savings rate when

- You receive a pay rise — save at least 50% of the increase

- You pay off a debt — redirect those payments into savings

- A large expense ends — such as a car loan or lease finishing

- You move to a cheaper living situation

- You get a windfall — bonus, tax refund, inheritance, or gift

It may be acceptable to temporarily reduce your savings when

- You face a genuine financial emergency

- You are between jobs and managing cash flow carefully

- You have an unusually high one-off expense that month

The key word is temporarily. Get back to your target savings rate as quickly as possible.

Common Mistakes People Make With Monthly Savings

Saving what is left instead of saving first

The most common mistake. If you wait to see what is left at the end of the month before saving, there is usually nothing left. Always save first on payday, then spend what remains.

Keeping all savings in one account

When your emergency fund, holiday savings, and house deposit are all mixed in one account, you lose track of progress and are more likely to spend from the wrong pot. Use separate labelled accounts for each goal.

Setting a savings goal with no deadline

I want to save $10,000″ is not a plan. “I want to save $10,000 in 18 months by putting $556 away each month” is a plan. Always attach a timeline to every savings goal.

Final Thoughts

How much money should you save each month? At minimum, aim for 20% of your take-home pay divided across your emergency fund, retirement, and specific goals. If that is not possible today, start with 5% and grow from there.

The most important thing is not the percentage — it is the habit. Consistent monthly saving, even at a small amount, builds the financial foundation that everything else rests on.

For more on building your monthly budget and reducing what you spend so you can save more, read our complete guide on budgeting for beginners [LINK TO PILLAR 3] and how to reduce monthly expenses.

What percentage of your income do you currently save? Let us know in the comments — and if you have a tip that helped you save more, share it below.

About the Author

James Carter writes about personal finance and smart money habits at GetWorldInfo.com. With over a decade of experience helping families budget smarter and cut everyday costs, James believes that saving money doesn’t require sacrifice — just the right strategy.

{kind=link}

Comments are off for this post.