Key Takeaways

Table of Contents

- The Simple Formula — How Long Will Your Money Last?

- The basic formula

- The more accurate version — accounting for interest

- How Long Will My Money Last If I Am Between Jobs?

- How to calculate your job loss runway

- Example — job loss scenario

- Tips to extend your runway during job loss

- How Long Will My Money Last in Retirement?

- The 4% rule — the most widely used retirement guideline

- How to work out if you have enough saved for retirement

- How Long Will My Money Last on a Fixed Income?

- The formula for fixed income situations

- Example — fixed income with a monthly deficit

- What Is a Burn Rate and Why Does It Matter?

- How to calculate your monthly burn rate

- How reducing your burn rate extends your money

- 8 Proven Ways to Make Your Money Last Longer

- 1. Cut your biggest expenses first

- 2. Move to a high-interest savings account

- 3. Eliminate unused subscriptions

- 4. Reduce grocery spending

- 5. Negotiate your bills

- 6. Generate some income while drawing down savings

- 7. Delay large non-essential purchases

- 8. Review your plan every month

- Common Mistakes That Make Your Money Run Out Faster

- Underestimating monthly expenses

- Ignoring irregular expenses

- Not adjusting for inflation

- Withdrawing from retirement accounts early

- Final Thoughts

- Having a clear picture of your burn rate is the first step to taking control of your finances

- How long your money lasts depends entirely on how much you have and how much you spend each month

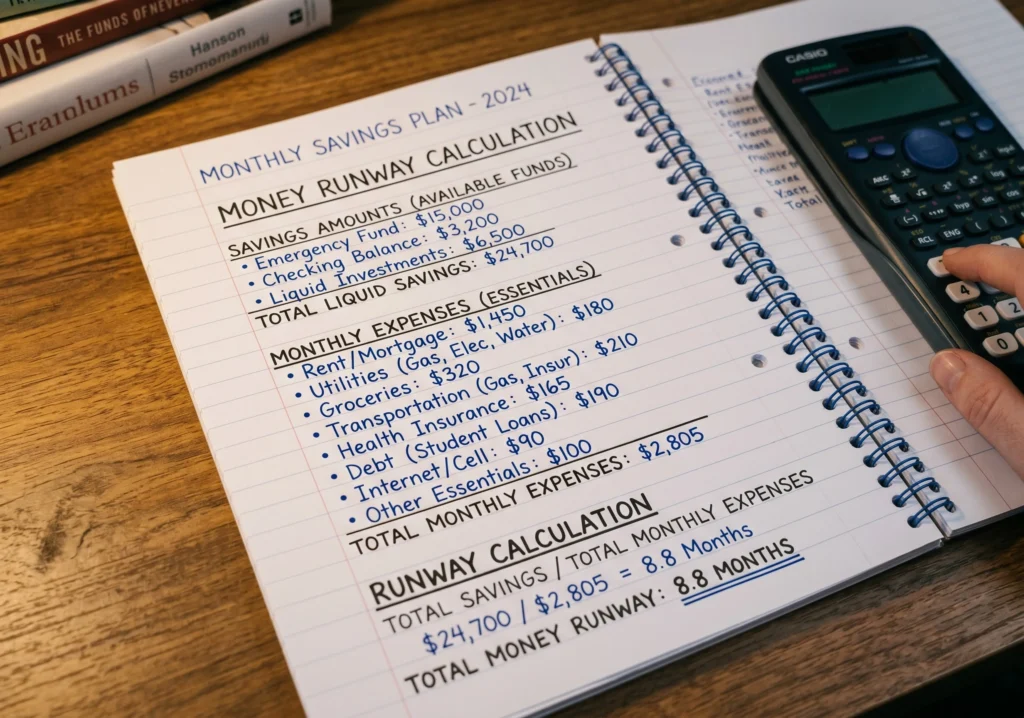

- The simple formula is: Total Savings ÷ Monthly Expenses = Months Your Money Will Last

- Reducing your monthly expenses is the most powerful lever for making your money last longer

- Interest earned on savings can significantly extend how long your money lasts

Whether you are between jobs, living off savings, planning for retirement, or simply trying to understand your financial runway — knowing how long your money will last is one of the most important calculations you can make. This guide walks you through the exact formula, a worked example for every situation, and proven strategies to make your money stretch further.

The Simple Formula — How Long Will Your Money Last?

The core calculation is straightforward. You need just two numbers — how much money you have and how much you spend each month.

The basic formula

Total Savings ÷ Monthly Expenses = Number of Months Your Money Will Last

Here are some worked examples:

- $10,000 saved · $2,000/month expenses → lasts 5 months

- $10,000 saved · $1,500/month expenses → lasts 6.6 months

- $25,000 saved · $2,000/month expenses → lasts 12.5 months

- $50,000 saved · $2,500/month expenses → lasts 20 months

- $100,000 saved · $3,000/month expenses → lasts 33 months (just under 3 years)

- $500,000 saved · $3,500/month expenses → lasts approximately 11.9 years

Find your own numbers in this formula and you instantly know your financial runway.

The more accurate version — accounting for interest

If your savings are sitting in a high-interest savings account, your money lasts slightly longer because it earns interest while you draw it down. The exact calculation gets complex but a rough rule of thumb is:

- At 3% annual interest on $50,000 → earns approximately $125/month in interest

- This effectively reduces your monthly drawdown by $125

- Meaning $2,500/month expenses become effectively $2,375/month when interest is factored in

Always factor in interest earnings when calculating your real runway — especially for larger amounts.

How Long Will My Money Last If I Am Between Jobs?

Being between jobs is one of the most common reasons people ask this question. Knowing your runway gives you clarity and removes panic from the situation.

How to calculate your job loss runway

- Add up your total savings and any redundancy or severance pay you received

- Calculate your essential monthly expenses only — rent, food, utilities, transport, insurance

- Remove all non-essential spending from your budget immediately

- Divide your total funds by your lean monthly expenses

Example — job loss scenario

Savings: $15,000 Redundancy pay: $5,000 Total funds: $20,000

Essential monthly expenses:

- Rent: $900

- Food: $300

- Utilities: $150

- Transport: $100

- Insurance: $100

- Total: $1,550/month

$20,000 ÷ $1,550 = 12.9 months of runway

This person has almost 13 months to find a new job before their money runs out — far more breathing room than most people assume they have once they do the calculation properly.

Tips to extend your runway during job loss

- Cancel all non-essential subscriptions immediately

- Apply for any unemployment benefits you are entitled to — this extends your runway significantly

- Pick up part-time or freelance work to slow the drawdown of your savings

- Negotiate a payment plan on any large bills rather than paying lump sums

- Avoid touching any retirement savings if at all possible — early withdrawal penalties are severe

How Long Will My Money Last in Retirement?

Retirement planning is the most common context for this question. Running out of money in retirement is one of the biggest financial fears people have — and it is entirely preventable with the right planning.

The 4% rule — the most widely used retirement guideline

The 4% rule states that you can withdraw 4% of your retirement savings per year and your money will last at least 30 years based on historical market returns.

Here is what that means in practice:

- $250,000 saved → 4% = $10,000/year ($833/month)

- $500,000 saved → 4% = $20,000/year ($1,667/month)

- $750,000 saved → 4% = $30,000/year ($2,500/month)

- $1,000,000 saved → 4% = $40,000/year ($3,333/month)

- $1,500,000 saved → 4% = $60,000/year ($5,000/month)

If your retirement expenses are higher than what 4% of your savings covers, you either need to save more before retiring or reduce your planned retirement expenses.

How to work out if you have enough saved for retirement

- Estimate your annual retirement expenses honestly

- Multiply that number by 25 — this is how much you need saved to follow the 4% rule safely

- Example: $40,000/year in expenses × 25 = $1,000,000 needed

This is called the 25x rule and it is the simplest way to set your retirement savings target.

How Long Will My Money Last on a Fixed Income?

If you are living on a fixed income — such as a pension, disability benefit, or investment income — the calculation is slightly different because you have ongoing income coming in alongside your savings.

The formula for fixed income situations

(Monthly Income – Monthly Expenses) = Monthly Surplus or Deficit

If your income covers your expenses with a surplus — your savings are untouched and continue to grow. If your income does not cover your expenses — you are drawing down savings each month.

Example — fixed income with a monthly deficit

Monthly pension income: $1,800 Monthly expenses: $2,300 Monthly deficit: $500

Savings: $60,000

$60,000 ÷ $500/month deficit = 120 months = 10 years before savings run out

In this situation the person has 10 years before their savings are depleted — assuming their pension income and expenses stay constant. Reducing expenses by $200/month would extend that to 25 years.

What Is a Burn Rate and Why Does It Matter?

Your burn rate is simply how much money you spend each month. It is the single most important number in determining how long your money lasts — and it is the one variable entirely within your control.

How to calculate your monthly burn rate

- Add up every outgoing payment from the last three months

- Divide the total by three

- That is your average monthly burn rate

Most people are surprised by how high their burn rate actually is when they calculate it properly. Subscription creep, dining out, and impulse spending are the biggest culprits.

How reducing your burn rate extends your money

Using the basic formula — $30,000 saved:

- At $2,000/month burn rate → lasts 15 months

- At $1,750/month burn rate → lasts 17.1 months

- At $1,500/month burn rate → lasts 20 months

- At $1,200/month burn rate → lasts 25 months

Reducing your monthly spending by just $500 adds 10 months to your runway. That is the power of controlling your burn rate.

8 Proven Ways to Make Your Money Last Longer

Once you know how long your money will last, the next question is how to extend that timeline. These strategies work whether you are between jobs, in retirement, or simply trying to make your savings go further.

1. Cut your biggest expenses first

The biggest impact comes from tackling your biggest expenses — not cutting out small luxuries. Rent, transport, and food account for the majority of most people’s spending. Even a modest reduction in these areas adds months to your runway.

2. Move to a high-interest savings account

If your savings are sitting in a standard account earning near-zero interest, you are leaving money on the table. Moving to a high-yield savings account earning 4–5% interest can add hundreds of dollars per year to your balance with zero effort.

3. Eliminate unused subscriptions

Go through your bank statement line by line and cancel every subscription you do not use weekly. Streaming services, gym memberships, software subscriptions, and premium apps add up to $100–$300 per month for most households.

4. Reduce grocery spending

Food is one of the most controllable expenses in your budget. Meal planning, switching to store brands, and reducing food waste can cut your grocery bill by 20–30% without eating less. Read our full guide on how to save money on groceries for a detailed breakdown.

5. Negotiate your bills

Call your internet, phone, and insurance providers and ask for a better rate. Most companies have retention deals they do not advertise. A single phone call can save $20–$50 per month on each bill — that is $240–$600 per year from one conversation.

6. Generate some income while drawing down savings

Even a small amount of part-time or freelance income dramatically extends how long your money lasts. Earning $500 per month from a side hustle while spending $2,000 per month is the equivalent of having $6,000 more in savings for every year you continue. See our guide on side hustle ideas for beginners for easy options.

7. Delay large non-essential purchases

When your money needs to last as long as possible, postpone any large non-essential purchases. A car upgrade, home renovation, or expensive holiday can wait until your financial situation is more stable.

8. Review your plan every month

Your burn rate, income, and savings balance all change over time. Set a monthly reminder to recalculate how long your money will last and adjust your spending accordingly. A monthly review catches problems early — before they become crises.

Common Mistakes That Make Your Money Run Out Faster

Underestimating monthly expenses

Most people underestimate what they actually spend each month by 20–30%. Always use your real bank statement figures — not what you think you spend.

Ignoring irregular expenses

Annual bills, car servicing, medical costs, and seasonal expenses do not show up every month but they are real costs. Divide them by 12 and add them to your monthly burn rate for an accurate picture.

Not adjusting for inflation

If you are planning over a long period — such as retirement — your expenses will increase with inflation over time. Factor in a 2–3% annual increase in expenses for any plan covering more than five years.

Withdrawing from retirement accounts early

Early withdrawal from retirement accounts typically triggers a 10% penalty plus income tax on the amount withdrawn. This can cost you 30–40% of the money you withdraw. Exhaust all other options before touching retirement savings.

Final Thoughts

Knowing how long your money will last is not about creating anxiety — it is about creating clarity. When you know your exact financial runway, you can make informed decisions, plan with confidence, and take the right steps to extend that runway if needed.

Use the simple formula — Total Savings ÷ Monthly Expenses — to calculate your number today. Then focus on the one lever that matters most: reducing your monthly burn rate.

For practical ways to cut your monthly expenses and make your money last longer, read our guides on how to reduce monthly expenses [LINK TO POST #8] and how much money should you save each month.

What is your biggest concern about making your money last? Leave a comment below — we read and respond to every one.

About the Author

James Carter writes about personal finance and smart money habits at GetWorldInfo.com. With over a decade of experience helping families budget smarter and cut everyday costs, James believes that saving money doesn’t require sacrifice — just the right strategy.

{kind=link}

No Comments