Key Takeaways

Table of Contents

- Step 1: Work Out Exactly How Much You Need

- How to calculate your deposit target

- Don’t forget the additional costs

- Step 2: Set a Realistic Savings Timeline

- How to build your savings timeline

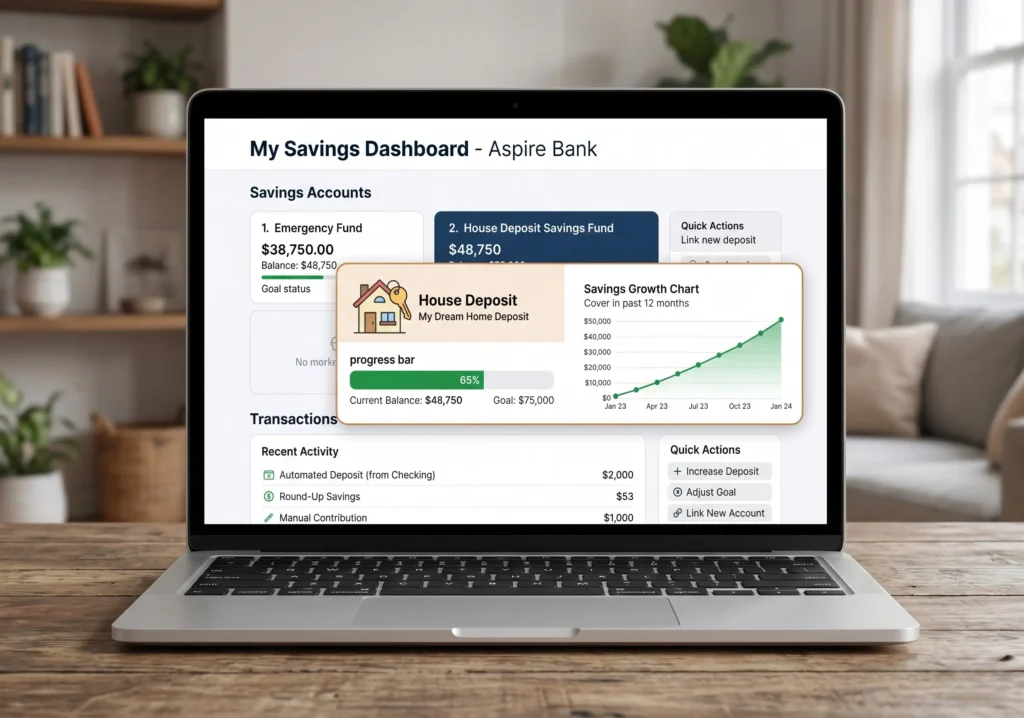

- Step 3: Open a Dedicated House Deposit Account

- What to look for in a savings account

- Step 4: Audit Your Monthly Expenses

- Common expenses to cut when saving for a house

- The 50/30/20 rule adjusted for house saving

- Step 5: Increase Your Income Where Possible

- Ways to boost your income while saving for a house

- Step 6: Check Government First-Home Buyer Schemes

- Examples of first-home buyer assistance schemes

- Step 7: Track Your Progress Every Month

- Simple ways to track your house deposit progress

- Step 8: Avoid These Common Saving Mistakes

- How Long Does It Realistically Take to Save for a House?

- Final Thoughts

- Most first-time buyers need a 5–20% deposit depending on their lender

- Opening a dedicated savings account for your deposit is a must

- Cutting just 3–4 monthly expenses can add thousands to your deposit per year

- A clear savings timeline keeps you motivated and on track

- Government first-home buyer schemes can significantly reduce how much you need to save

Saving for a house feels overwhelming until you break it into a clear system. Whether you need $20,000 or $100,000 for your deposit, the process is the same — you need a target, a timeline, and a plan to cut the gap between your income and your savings rate. This guide walks you through every step.

Step 1: Work Out Exactly How Much You Need

Before you save a single dollar, you need a number to aim for. Without a target, saving for a house feels endless.

How to calculate your deposit target

Most lenders require a deposit of between 5% and 20% of the property’s purchase price. A 20% deposit is ideal because it avoids paying private mortgage insurance (PMI), which adds hundreds of dollars to your monthly payments.

Here’s a simple breakdown:

- $200,000 home → 10% deposit = $20,000 · 20% deposit = $40,000

- $350,000 home → 10% deposit = $35,000 · 20% deposit = $70,000

- $500,000 home → 10% deposit = $50,000 · 20% deposit = $100,000

Don’t forget the additional costs

Beyond the deposit, budget for these one-off costs:

- Stamp duty or transfer tax (varies by state/country)

- Legal and conveyancing fees ($1,000–$3,000)

- Home inspection fees ($300–$600)

- Moving costs ($500–$2,000)

Add 3–5% of the purchase price on top of your deposit target to cover these comfortably.

Step 2: Set a Realistic Savings Timeline

Once you have your target number, work backwards to create a timeline. This turns a vague goal into a monthly savings plan.

How to build your savings timeline

Divide your deposit target by the number of months you want to save:

- Target: $40,000 · Timeline: 3 years (36 months) = $1,111 per month

- Target: $40,000 · Timeline: 4 years (48 months) = $834 per month

- Target: $40,000 · Timeline: 5 years (60 months) = $667 per month

Pick the timeline that results in a monthly savings amount you can realistically achieve without completely sacrificing your lifestyle. Then stick to it like a bill you must pay.

Step 3: Open a Dedicated House Deposit Account

Never mix your house deposit savings with your everyday spending account. Open a separate high-interest savings account specifically for your deposit and treat it as untouchable.

What to look for in a savings account

- High interest rate (every bit of interest shortens your timeline)

- No monthly fees

- Limited or no easy withdrawal access (friction is your friend here)

- Government-backed deposit protection

Set up an automatic transfer into this account on the same day your salary lands. Pay your future home first, then live on what’s left.

Step 4: Audit Your Monthly Expenses

To hit your savings target every month, something has to give. Go through your last three months of bank statements and identify every non-essential expense.

Common expenses to cut when saving for a house

- Streaming subscriptions you rarely use ($10–$50/month each)

- Dining out and takeaways (average household spends $200–$400/month)

- Gym memberships you don’t fully use ($30–$100/month)

- Unused app subscriptions and free trials that rolled into paid plans

- Impulse online shopping (unsubscribe from retail email lists immediately)

Cutting just three of these can free up $200–$400 per month — that’s $2,400–$4,800 extra toward your deposit every year.

The 50/30/20 rule adjusted for house saving

If you’re serious about saving for a house, temporarily adjust the classic 50/30/20 budget:

- 50% on needs (rent, food, transport, utilities)

- 20% on wants (dining, entertainment, shopping) — reduced from 30%

- 30% on savings — increased from 20%

This one shift can cut years off your savings timeline.

Step 5: Increase Your Income Where Possible

Cutting expenses speeds up your savings — but increasing your income accelerates it even faster. Even an extra $300–$500 per month goes straight to your deposit.

Ways to boost your income while saving for a house

- Take on freelance work in your field on weekends

- Sell unused items at home (furniture, clothes, electronics)

- Pick up overtime hours at your current job

- Rent out a spare room if you’re currently renting

- Start a side hustle that fits around your schedule

For a full breakdown of the best options, read our guide on the best freelance side hustles you can start this week.

Step 6: Check Government First-Home Buyer Schemes

Many countries offer government programmes specifically designed to help first-time buyers save faster or borrow with a smaller deposit. These are genuinely worth researching before assuming you need the full 20%.

Examples of first-home buyer assistance schemes

- USA: FHA loans allow deposits as low as 3.5%

- UK: Lifetime ISA gives a 25% government bonus on savings up to £4,000/year

- Australia: First Home Super Saver Scheme allows saving inside your super fund

- Canada: First Home Savings Account offers tax-free savings up to $40,000

Check what’s available in your country — the right scheme can save you tens of thousands or shorten your timeline by years.

Step 7: Track Your Progress Every Month

Saving for a house is a long game. Without regular check-ins, motivation fades and spending creeps back up. Set a monthly money date with yourself — 15 minutes to review your savings balance, check you hit your target, and adjust if needed.

Simple ways to track your house deposit progress

- Use a free app like Mint or YNAB to track savings automatically

- Keep a simple spreadsheet with your monthly target vs actual savings

- Set a milestone reward for every 25% of your deposit saved — something small and meaningful that keeps you motivated

Step 8: Avoid These Common Saving Mistakes

Even people with good savings habits make these mistakes when saving for a house.

Mistakes that slow down your house deposit savings

- Dipping into the savings account for non-emergencies — this is why a separate account matters

- Not accounting for inflation in property prices — revisit your target annually

- Saving without a timeline — vague goals produce vague results

- Waiting until you feel “ready” to start — every month you delay costs you more in rising property prices

- Keeping savings in a low-interest account — even a 1% difference in interest rate makes thousands of dollars difference over 5 years

How Long Does It Realistically Take to Save for a House?

This depends entirely on your income, your target deposit, and how aggressively you save. For most first-time buyers saving a 10–20% deposit on a median-priced home, the realistic timeline is 3–7 years with consistent effort.

The key is to start now, automate your savings, and revisit your plan every few months. Every month you delay is a month of compound interest you’re missing — and in most markets, a month of rising property prices eating into your goal.

Final Thoughts

Knowing how to save money for a house is really about building a system — a target, a timeline, a dedicated account, and monthly habits that keep you on track. None of these steps are complicated individually. The challenge is doing all of them consistently.

Start with Steps 1, 2, and 3 today. Get your number, build your timeline, and open that dedicated account. Everything else follows from there.

Want to reduce your monthly expenses even further to hit your savings target faster? Read our guide on how to save money on groceries and how to reduce your monthly expenses — together they can free up hundreds of dollars every month toward your deposit.

About the Author

James Carter writes about personal finance and smart money habits at GetWorldInfo.com. With over a decade of experience helping families budget smarter and cut everyday costs, James believes that saving money doesn’t require sacrifice — just the right strategy.

{kind=link}

No Comments