Key Takeaways

Table of Contents

- Why Most People Fail to Save from Their Salary

- Reason 1 — They save last instead of first

- Reason 2 — They have no clear savings target

- Reason 3 — They have not automated it

- Step 1 — Know Your Exact Monthly Take-Home Pay

- How to calculate your real take-home pay

- Step 2 — Calculate Your Monthly Essential Expenses

- What counts as an essential expense

- What does not count as essential

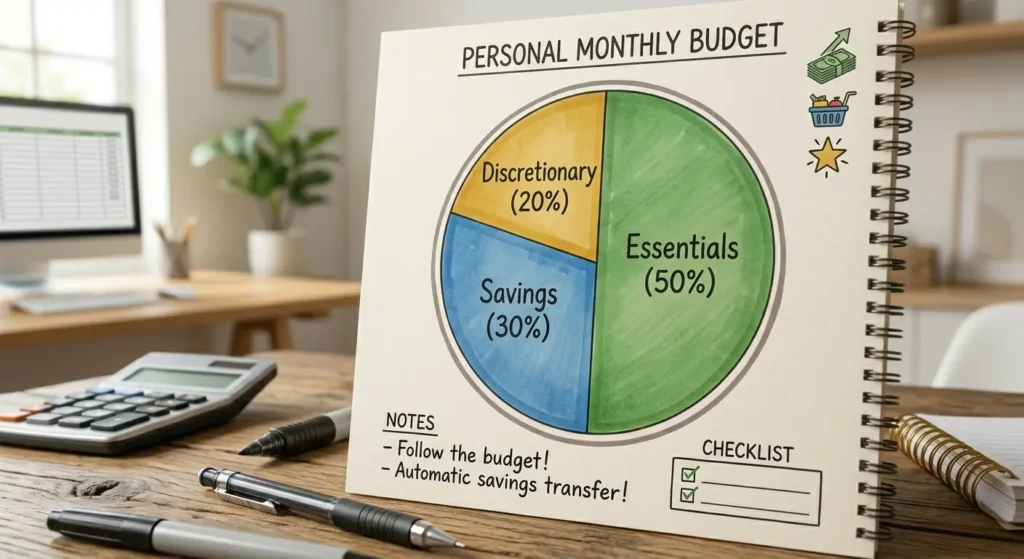

- Step 3 — Decide How Much of Your Salary to Save

- Recommended savings percentages by situation

- A practical example

- What if there is nothing left after essentials

- Step 4 — Open a Dedicated Savings Account

- What to look for in a salary savings account

- Step 5 — Automate Your Savings on Payday

- How to set up automatic salary savings in 3 steps

- Step 6 — Apply the Pay Yourself First Rule

- How pay yourself first works in practice

- Step 7 — Handle Salary Increases the Right Way

- The 50/50 rule for salary increases

- Example — applying a pay rise

- Step 8 — Review Your Savings Rate Every 3 Months

- Signs it is time to increase your savings rate

- Common Mistakes People Make When Saving from Their Salary

- Saving an irregular amount each month

- Using savings for non-emergencies

- Waiting until the salary feels big enough to save

- Keeping savings in a zero-interest account

- How Much Will You Have If You Start Saving Now?

- Final Thoughts

- The most important rule is to save first on payday — before spending anything

- Even saving 10% of your salary consistently builds significant wealth over time

- Automating your savings removes the willpower required and makes it effortless

- Knowing your exact monthly expenses is essential before you can build a savings habit

- Small consistent savings beat large irregular ones every single time

Most people plan to save whatever is left at the end of the month. Most people save nothing. The single biggest shift you can make is deciding to save first and spend what remains — not the other way around. This guide shows you exactly how to build a system that saves money from your salary every single month, regardless of how much you earn.

Why Most People Fail to Save from Their Salary

Before building the solution it helps to understand the problem. There are three reasons most people consistently fail to save from their salary — and none of them are about not earning enough.

Reason 1 — They save last instead of first

When you wait until the end of the month to save whatever is left, there is almost never anything left. Lifestyle spending, impulse purchases, and unexpected costs absorb every spare dollar before savings ever get a chance. Saving last is the single biggest reason people with decent salaries still have nothing put away.

Reason 2 — They have no clear savings target

Wanting to save money is not a plan. Saving $400 on the 1st of every month into a dedicated account is a plan. Without a specific number attached to a specific action on a specific date, saving remains an intention rather than a habit.

Reason 3 — They have not automated it

Relying on willpower to transfer money to savings every month guarantees inconsistency. Some months it happens, most months it does not. Automation removes the decision entirely — the money moves before you can spend it.

Step 1 — Know Your Exact Monthly Take-Home Pay

Before you can decide how much to save you need to know exactly how much you bring home after tax, pension contributions, and any other deductions.

How to calculate your real take-home pay

- Check your most recent payslip for your net pay figure — this is what actually lands in your bank account

- If your income varies month to month, take your last three months of net pay and calculate the average

- Add any reliable additional income — regular overtime, side hustle income that comes in every month

- Do not include irregular bonuses or one-off payments in your baseline — these are a bonus, not something to rely on

Write this number down. This is your monthly starting point for everything that follows.

Step 2 — Calculate Your Monthly Essential Expenses

Your essential expenses are the non-negotiable costs you must cover every month. These come before savings in your budget — but nothing else does.

What counts as an essential expense

- Rent or mortgage payment

- Utility bills — electricity, gas, water, internet

- Groceries and basic food

- Transport costs — fuel, public transport, car insurance and road tax

- Minimum debt repayments — credit cards, loans, student debt

- Essential insurance — health, home, life

Add these up and subtract them from your take-home pay. What remains is your discretionary income — the money available for savings and non-essential spending.

What does not count as essential

- Streaming subscriptions

- Dining out and takeaways

- Gym memberships

- Shopping and clothing beyond basics

- Entertainment

These are wants, not needs. They come after your savings transfer — not before.

Step 3 — Decide How Much of Your Salary to Save

Once you know your take-home pay and your essential expenses, you can set a specific monthly savings amount. The right number depends on your income and current financial situation.

Recommended savings percentages by situation

- Just starting out or in debt: save 5–10% of take-home pay as a starting point

- Stable income, no high-interest debt: save 15–20% of take-home pay

- Aggressively building toward a goal (house deposit, emergency fund): save 25–30% if possible

- The absolute minimum to start: even 3–5% is infinitely better than zero

A practical example

Take-home pay: $3,500/month Essential expenses: $2,100/month Discretionary income: $1,400/month Savings target at 15%: $525/month Remaining for non-essential spending: $875/month

This leaves nearly $900 per month for dining out, entertainment, clothing, and personal spending — a very comfortable amount while still saving $6,300 per year.

What if there is nothing left after essentials

If your essential expenses consume almost all of your income, the savings conversation becomes a spending reduction conversation first. Read our guide on how to reduce monthly expenses which covers 12 specific ways to cut your essential and non-essential costs to free up money for savings.

Step 4 — Open a Dedicated Savings Account

Never keep your savings in the same account as your everyday spending. When savings and spending money share an account, the savings get spent. This is not a willpower problem — it is a design problem. Fix the design.

What to look for in a salary savings account

- Completely separate from your current or checking account

- High interest rate — shop around for the best available rate

- No monthly fees eating into your balance

- Ideally with limited easy access — some friction between you and the money is a feature, not a bug

- Name the account something specific — “House Deposit”, “Emergency Fund”, or “Future Me”

The psychological effect of a named, separate account is real. People consistently save more and dip in less when the account has a clear purpose attached to it.

Step 5 — Automate Your Savings on Payday

This is the most important step in the entire system. Set up an automatic transfer from your main account to your savings account that fires on the same day your salary arrives — ideally the same day or the day after.

How to set up automatic salary savings in 3 steps

- Log into your online banking

- Set up a standing order or automatic transfer to your savings account

- Set the amount to your monthly savings target

- Set the date to your payday or the day after

From this point forward the saving happens automatically. You never have to think about it, decide to do it, or remember to do it. Your salary arrives, the savings transfer fires, and you live on what remains. This is exactly how people who consistently save actually do it — not through willpower, but through automation.

Step 6 — Apply the Pay Yourself First Rule

Pay yourself first is the foundational principle behind every successful salary savings habit. It means treating your monthly savings transfer as the first bill you pay — not the last thing you do with what is left.

How pay yourself first works in practice

Traditional approach — salary arrives → pay bills → spend on wants → save whatever is left → usually nothing left

Pay yourself first approach — salary arrives → savings transfer fires automatically → pay bills → spend remaining on wants → nothing to save because it is already saved

The outcome is completely different. The second approach works because it removes the temptation to spend money that was never meant to be spent.

Step 7 — Handle Salary Increases the Right Way

Most people who get a pay rise immediately increase their lifestyle spending to match — and end up saving the same amount or less than before. This is called lifestyle inflation and it is one of the biggest obstacles to long-term wealth building.

The 50/50 rule for salary increases

When you receive a pay rise, split the increase equally:

- 50% goes to improving your lifestyle — it is okay to enjoy earning more

- 50% goes straight to increasing your monthly savings transfer

This way you genuinely benefit from earning more while simultaneously accelerating your savings. Every pay rise becomes a savings accelerator rather than just a lifestyle upgrade.

Example — applying a pay rise

Current salary: $3,500/month take-home Pay rise: $300/month additional take-home 50% lifestyle improvement: $150/month extra spending 50% savings increase: increase monthly savings transfer by $150

Over one year this increases your annual savings by $1,800 — from a pay rise you were going to spend entirely anyway.

Step 8 — Review Your Savings Rate Every 3 Months

Your financial situation changes over time. Debts get paid off, expenses change, income grows. Review your savings rate every three months and adjust upward whenever possible.

Signs it is time to increase your savings rate

- A debt has been paid off — redirect those payments to savings

- Your income has increased — apply the 50/50 rule

- A regular expense has ended — a car loan, lease, or subscription

- Your essential expenses have decreased — moved somewhere cheaper, switched providers

- You received a one-off windfall — tax refund, bonus, gift — put at least 50% into savings

Each time you increase your savings rate even slightly, the compounding effect over months and years is significant.

Common Mistakes People Make When Saving from Their Salary

Saving an irregular amount each month

Saving $600 one month and $50 the next is not a savings habit — it is occasional saving. Consistency is the entire point. A fixed automatic transfer on a fixed date every month is the only approach that works long term.

Using savings for non-emergencies

Your savings account is not a float for when you overspend. If you find yourself regularly dipping into savings to cover everyday costs, the issue is that your non-essential spending budget is too high — not that your savings are there to be used.

Waiting until the salary feels big enough to save

There is no salary level at which saving becomes easy if you have not built the habit. People earning $30,000 per year who save consistently build more wealth than people earning $80,000 who save nothing. Start with whatever you can — the habit matters far more than the amount.

Keeping savings in a zero-interest account

Money sitting in a standard account earning near-zero interest is losing value to inflation every month. Move your savings to a high-interest account immediately — the difference over a year or two is hundreds of dollars.

How Much Will You Have If You Start Saving Now?

Here is what consistent monthly saving from your salary looks like over time at a 4% annual interest rate:

- Save $200/month for 5 years → approximately $13,300

- Save $300/month for 5 years → approximately $19,900

- Save $500/month for 5 years → approximately $33,200

- Save $500/month for 10 years → approximately $73,700

- Save $1,000/month for 10 years → approximately $147,400

The longer you save consistently, the more interest compounds and accelerates your total. Starting today — even at a small amount — always beats waiting until the amount feels significant.

Final Thoughts

Saving money from your salary every month is not complicated. It comes down to one decision made once — automate a transfer to a dedicated savings account on payday — and then leaving that system alone to work.

Decide your savings amount today. Open a dedicated account if you do not already have one. Set up the automatic transfer. Then do not touch it.

For more ways to make your savings go further, read our guide on how much money should you save each month to make sure your savings rate aligns with your goals — and our complete guide on how to save money [LINK TO PILLAR 1 — add when live] which covers every savings situation in one place.

What percentage of your salary do you currently save? Let us know in the comments — and share any tips that have helped you save more consistently.

About the Author

Alex Mitchell writes about personal finance and smart money habits at GetWorldInfo.com. With over a decade of experience helping families budget smarter and cut everyday costs, James believes that saving money doesn’t require sacrifice — just the right strategy.

{kind=link}

No Comments